1

WASHINGTON STATE DEPARTMENT OF REVENUE

In Washington state, all real and personal property is

subject to tax unless specically exempted by law.

Property tax was the rst tax levied in the state of

Washington. Today, property tax accounts for about

30% of total state and local taxes. It connues to be the

most important revenue source for public schools, re

protecon, libraries, and parks and recreaon.

The informaon contained in this publicaon is current

at the me of producon. However, state tax laws, their

interpretaon, and their applicaon can change because

of legislave acon, reviews, or court decisions. This

publicaon will not reect these changes.

Property values

State law requires that assessors appraise property at

100% of its true and fair market value in money, according

to the highest and best use of the property. Fair market

value, or true value, is the amount of money that a willing

and unobligated buyer is willing to pay a willing and

unobligated seller.

Real property

Real property includes land, improvements to land,

structures, and certain equipment axed to structures.

Characteriscs of real property that inuence the value

include but are not limited to zoning, locaon, view,

geographic features, easements, covenants, and the

condion of surrounding properes.

The assessor values real property using one or more of

the following appraisal methods:

• Market or sales comparison approach to value is

determined, or esmated, based on mulple sales of

similar properes. Most residenal property is valued

using this method.

• Cost approach to value is determined based on the

cost of replacing an exisng structure with a similar

one that serves the same purpose. This method is

commonly used to value new construcon.

• Income approach to value is determined based on the

income producing potenal of the property. This

method is used primarily to value business property.

Personal property

The primary characterisc of personal property is

mobility. Personal property includes furnishings,

machinery and equipment, xtures, supplies, and tools.

Most personal property owned by individuals is

specically exempt. However, if these items are used in

a business, personal property tax applies. For detailed

informaon about personal property tax, please refer to

the Personal Property Tax publicaon.

Changes to property values

All counes revalue properes each year and are required

to do physical inspecons at least once every six years.

If your appraised property value changes, you will receive

a change of value noce that lists the old and new

appraised value of land and improvements. By comparing

the two values, you can determine if your appraised

property value has increased or decreased.

The assessed value of your property may be less than the

appraised value if you are receiving any type of property

tax exempon or reducon.

Valuaon noces are not tax bills. An increase in value

does not necessarily mean that next year’s property taxes

will increase at a proporonate rate.

Homeowner’s Guide to

Property Tax

This fact sheet provides general informaon about Washington’s

property tax. For more informaon or to get answers to specic

quesons, please contact your local county assessor’s oce.

JUNE 2023

2

WASHINGTON STATE DEPARTMENT OF REVENUE

Property tax rates and limitaons

Property tax rates are expressed in dollars per thousand

dollars of assessed property value. Assessors set the

levy rate based on the taxing district’s budget request,

the total assessed value of the taxing district, and any

applicable levy limitaons.

Property tax levy limitaons restrict or limit increases to

property tax rates. Two such limitaons include the One-

Percent Constuonal Limit and the Levy Limit.

The 1% constuonal limit

Washington State’s Constuon limits the regular (non-

voted) combined property tax rate that applies to an

individual’s property to 1% of market value ($10 per

$1,000). Voter approved special levies, such as special

levies for schools, are in addion to this amount.

The levy limit

The levy limit applies to a taxing district’s levy amount,

and not to increases in the assessed value of individual

properes. The limit is based on the populaon of the

district as well as the district’s need to increase revenue.

The law restricts taxing districts from levying, in any year,

more than a 1% increase in its regular, non-voted levy

over the highest amount that could have been levied since

1985.

A taxing district with a populaon below 10,000 must

adopt a resoluon/ordinance to be able to increase its

levy up to the 1% limit.

Taxing districts with a populaon of 10,000 or more are

limited to the lesser of 1% or the rate of inaon with the

adopon of a resoluon/ordinance. If the rate of inaon

is less than one percent, the district could increase its

levy up to the 1% limit if it can show substanal need for

addional funds and its governing board passes a second

resoluon/ordinance.

Because the levy limit does not include new construcon,

annexaons, and voter approved excess levies, a taxing

district’s actual revenue increase may be greater than 1%.

Appeal of true and fair market value

If you do not agree with the assessed value of your

property, you are encouraged to contact your local county

assessor’s oce. You can nd a full list here: dor.wa.gov/

CountyContacts.

Disagreements of property values are oen seled at this

level. You may request copies of the comparable sales

informaon the assessor used to value your property.

If you are unable to reach an agreement, you may le an

appeal with the county board of equalizaon (BOE) in the

county where the property is located. Appeal forms are

available at the assessor’s oce, BOE oce or

dor.wa.gov/forms-publicaons/forms-subject/property-

tax-forms#Appeals

The completed peon must be led with the BOE by July

1 of the assessment year you are appealing or within 30

days of the date the change of value noce was mailed,

whichever date is later. Some counes have extended

the ling deadline up to 60 days. Please check with the

Board of Equalizaon in the county where the property is

located to determine your ling deadline.

If you or the assessor disagrees with the BOE

determinaon, their decision can be appealed to the State

Board of Tax Appeals (BTA). If the appeal at the BTA is a

“formal” appeal compared to an “informal” appeal, the

decision made by the BTA can be appealed in Superior

Court.

Informaon needed to appeal

The appeal form must include specic reasons why you

believe the assessor’s valuaon is incorrect. Examples may

include an appraisal of your property as of the assessment

date in queson, excessive deterioraon of your property

or sales of similar properes reecng a lower value for

your property. Statements that the assessor’s valuaon is

too high or property taxes are excessive are not sucient

reasons.

For a successful appeal, you must provide market

evidence that clearly shows the assessor’s valuaon is

incorrect. This evidence may include informaon on sales

of comparable properes in your area or documentaon

about condions of the property that the assessor may

not have known. For example, the land is not suitable for

a sepc system or is not suitable for a building site.

If you have any quesons about appeal procedures,

please contact your local BOE or the assessor’s oce. The

telephone numbers are listed in the county government

secon of the telephone directory.

You must provide market evidence that the

assessed value does not reect true and fair market

value.

3

WASHINGTON STATE DEPARTMENT OF REVENUE

Property tax rates vary

Many factors determine property tax rates, the amount

of property tax due on comparable properes will

vary throughout a county. The three main factors that

determine the tax rate include:

• Various combinaons of taxing districts in dierent

areas of the county.

• Budget amounts for each taxing district.

• Voter-approved special levies

and bonds.

Calculang your taxes

If you know the assessed value of your property and

the tax levy rate, you can calculate the amount of tax.

For example, if the assessed value of your property is

$150,000 and the levy rate is $9.41 per thousand dollars

of value, your tax will be $1,411.50.

$150,000 x .00941 ($9.41 per $1,000)

$1,411.50 tax liability

How to pay your property taxes

Property tax statements are mailed by the county

treasurer in February of each year. To avoid interest and

penales, at least half of the amount due must be paid by

April 30 (if the tax is less than $50 it must be paid in full by

April 30) and the balance by October 31. You can pay your

property tax in person or by mail. Some counes are now

accepng electronic payments via the county treasurer

website. Check with your county treasurer to see if this

opon is available to you. When paying by mail, be sure to

write the tax parcel or account number on your check and

include the tax statement payment stub.

Many lending companies pay the property tax for the

homeowner from a property tax reserve account. In

this case, tax statements are sent directly to the lending

company. If your lending company pays the tax directly

and you would like to receive informaon, please contact

your local county treasurer’s oce.

Quesons

If you have quesons about paying your property taxes,

please contact your local county treasurer’s oce.

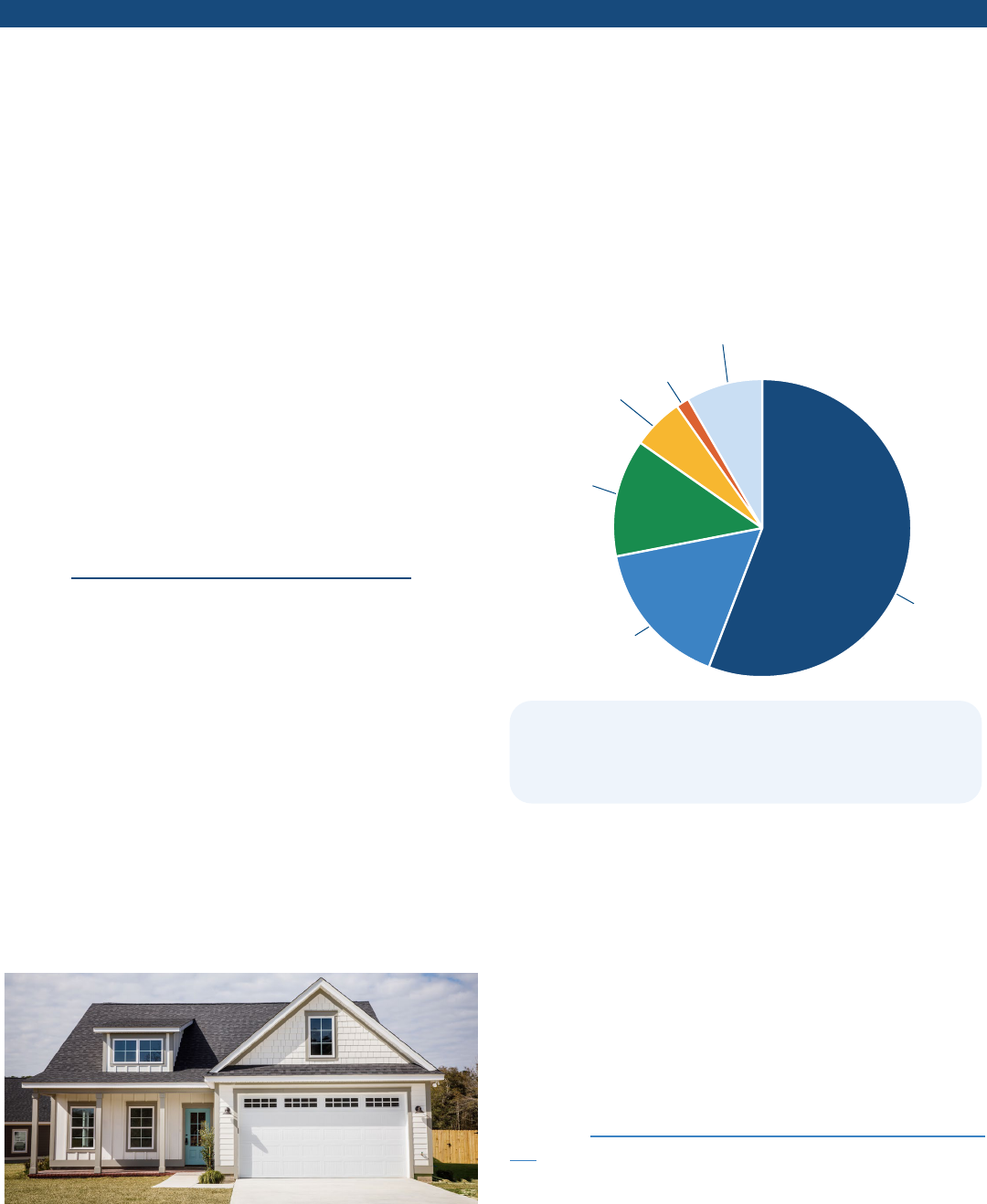

Where your property tax money goes

Reducons, exempons, deferrals and

assistance

Reducons

Destroyed property

Any real or personal property that has been destroyed

in whole or part, or is in an area that has been declared

a disaster area by the governor or the county legislave

authority and has been reduced in value by more than

20% may be eligible for a property assessment reducon

and or abatement of property taxes. Destroyed property

form applicaons are available at your assessor’s oce or

on line at dor.wa.gov/sites/default/les/2022-02/64-0003.

pdf.

Current use program and designated forest land

Owners of agricultural, open space, mber land, or

designated forest land may qualify for a reduced

assessment under the current use program or as

designated forest land. However, addional tax, interest,

Ports

*Other

Schools

Counes

Cies &

Towns

Fire

* Other includes regional libraries, parks and recreaon,

emergency medical, and hospital districts. (Distribuon of 2015

tax year)

56%

16%

12.7%

5.5%

8.2%

1.5%

4

WASHINGTON STATE DEPARTMENT OF REVENUE

and penales or compensang tax may apply when

property is removed from classicaon.

Applicaons must be received by Dec. 31 for a reducon

in assessment the following year. Applicaon forms are

available through the assessor’s oce.

Exempons

Property tax exempon for senior cizens and disabled

persons

This program freezes the value of your residence (as

of January 1 of the inial year of applicaon), exempts

all excess levies, and may exempt a poron of regular

levies, thereby reducing the amount of property tax due.

Senior cizens, veterans with a 100% service-connected

disability, and disabled persons may qualify. Household

income determines eligibility and level of exempon. The

county assessor approves or denies applicaons for this

program.

Three-year tax exempon on value of remodel

If you improve your single family residence such as adding

a new room, deck, or pao, you may qualify for a three-

year tax exempon on the value of the improvements.

Normal maintenance does not qualify. To receive the

exempon, you must apply through your local county

assessor’s oce prior to beginning your remodeling

project.

Other exempon

Churches, government enes, and many nonprot

agencies are exempt from property tax if they use

property for a tax-exempt purpose. The Department of

Revenue determines which properes are entled to the

exempon based on laws enacted by the Legislature.

Deferrals

Under these programs, the state of Washington pays

all, or a poron, of your property taxes on your behalf.

Unlike the tax exempons, deferred taxes are a lien

on the property. The lien becomes payable, together

with interest, upon sale, transfer, or inheritance of the

property, or when the home is no longer your primary

residence. The county assessor approves or denies

applicaons for the deferral programs.

Property tax deferral program for senior cizens and

disabled persons

If qualied, you can defer your property taxes and special

assessments in an amount up to 80% of the equity in your

home. Senior cizens and disabled persons may qualify.

Household income and equity determine eligibility. The

current interest rate is set in statute and is 5%.

Property tax deferral program for homeowners with

limited income

If qualied, you can defer your second half property taxes,

due in October, in an amount up to 40% of the equity in

your home. There is no age or disability requirement but

you must have owned your home for at least ve years.

Household income and equity determine eligibility. The

interest rate varies annually, as provided in statute, and is

based on an average of the federal short-term rate, plus

2%.

Assistance

Property tax assistance for widows or widowers of

veterans

This program is a grant assistance program to help you

pay property taxes. Senior cizens and disabled persons

who are widows or widowers of a veteran may qualify.

Age or disability, household income, and your spouse’s

veteran status at the me of his/her death determine

eligibility for this program. The Department of Revenue

administers this program and approves or denies claims

for assistance.

5

WASHINGTON STATE DEPARTMENT OF REVENUE

PT0012 06/02/2023

Important dates to remember

January 1

Real and personal property is valued for taxes due next

year.

March 31

Applicaons due for Senior/Disabled Deferral and Widow/

Widower Assistance.

April 30

First half of property taxes due.

Personal Property lisng forms due to assessor.

May 1

1% per month (12% per annum) assessed on delinquent

taxes.

June 1

3% penalty assessed on current year’s delinquent taxes.

July 1

Deadline for appeals to the County Board of Equalizaon

on current year’s assessment; or 30 days from date of

nocaon, whichever is later.

August 31

New construcon placed on current assessment roll at the

valuaon assessed July 31.

September 1

Limited Income Deferral applicaons due.

October 31

Second half of property taxes due.

December 1

8% penalty assessed on current year's delinquent tax.

December 31

Current Use Program and Designated Forest Land

applicaons due.

Property tax exempon applicaons for senior cizens

and disabled persons due.

For general informaon, contact the

Department of Revenue

• Telephone Informaon Center, 360-705-6705.

• dor.wa.gov.

• For tax assistance or to request this document in an

alternate format, visit dor.wa.gov or call 360-705-

6705. Teletype (TTY) users may use the Washington

Relay Service by calling 711.

Need more informaon?

The following publicaons are available from your local

county assessor’s oce. You may also obtain a copy from

the Department of Revenue online at dor.wa.gov or by

calling 360-534-1400.

• Personal Property Tax.

• Nonprot Organizaons.

• Property Tax Deferrals for Senior Cizens and People

with Disabilies.

• Property Tax Deferrals for Homeowners With Limited

Income.

• Property Tax Exempons for Senior Cizens and

People with Disabilies.

• Assistance Program for Widows or Widowers of

Veterans.

• Open Space Taxaon Act.

• Appealing your Property Tax Valuaon to the County

Board of Equalizaon.

Quesons

Your local county assessor’s oce can answer quesons

regarding:

• Assessed values.

• Appeals.

• Personal property.

• Current Use Program and Designated Forest Land.

• Property Tax Deferrals for Senior Cizens and People

with Disabilies.

• Property Tax Deferrals for Homeowners With Limited

Income.

• Property Tax Exempons for Senior Cizens and

People with Disabilies.

Your local county treasurer’s oce can answer quesons

regarding:

• Tax statements.

• Paying property tax.